The Path to Seamless Blockchain-Based Retail Payments: The Role of Interoperability

BY THE AXELAR FOUNDATION AND THE STELLAR DEVELOPMENT FOUNDATION

With stablecoins poised for rapid growth as regulatory clarity emerges and financial institutions prepare new offerings, blockchain-based retail payments are closer than ever.

In 2008, Satoshi Nakamoto’s Bitcoin white paper envisioned a “peer-to-peer electronic cash system” designed to enable trustless, decentralized payments. Bitcoin was crafted with retail transactions in mind. Today, the cryptocurrency landscape has evolved dramatically, with dozens of blockchains like Ethereum, Solana and Stellar powering diverse applications. However, this proliferation has led to a fragmented ecosystem. Many blockchain networks operate in silos, with limited communication or compatibility, hindering the seamless retail payment experience that is the standard for digital payments online and in physical stores. Today, with stablecoins poised for rapid growth as regulatory clarity emerges and financial institutions prepare new offerings, blockchain-based retail payments are closer than ever. However, for blockchain-based retail payments to rival the convenience of traditional systems, interoperability – both within blockchain ecosystems and with existing payment infrastructure – is essential.

Interoperability in Traditional Retail Payments: A Well-Oiled Machine

To understand the interoperability needed for blockchain-based retail payments, the seamless interoperability that defines traditional retail payments is a helpful analogy. The retail payments stack comprises three key layers: payment instruments, payment networks and payment processors, each interacting to deliver a frictionless user experience.

Payment instruments: These are the tools consumers use to initiate payments, such as credit cards, debit cards, mobile apps (e.g., Apple Pay) or even cash. Each instrument is tied to a financial institution or payment provider, which authenticates and authorizes transactions.

Payment networks: These are the rails that facilitate transaction communication, such as Visa, Mastercard or SWIFT for international transfers. Payment networks ensure that funds move securely between the payer’s and payee’s financial institutions, standardizing protocols to enable interoperability across banks and regions.

Payment processors: Entities like Stripe, Square or PayPal act as intermediaries, handling the technical and regulatory complexities of transactions. They integrate with payment networks and financial institutions, ensuring merchants receive funds and consumers experience minimal friction.

Interoperability in this ecosystem is achieved through standardized protocols and interconnection points. For instance, a consumer using a Visa credit card issued by a U.S. bank can pay a merchant in Europe via a Mastercard-compatible point-of-sale terminal. Behind the scenes, payment networks and processors reconcile currency conversions, comply with regulations, and settle funds across discrete banking systems. Initiatives like ISO 20022, a global standard for payment messaging, further enhance interoperability by ensuring consistent data formats across networks. This seamless integration allows consumers to focus on their purchases, oblivious to the complex choreography of systems working together.

Blockchain Innovations in Retail Payments: The Stellar Example

Blockchain technology promises to disrupt retail payments by offering transparency, speed and cost efficiency. However, its potential is constrained by the lack of interoperability among blockchain networks and with traditional payment systems. Innovations like those developed by the Stellar network, as outlined at stellar.org/use-cases/payments, demonstrate how blockchain can address these challenges and pave the way for retail payment solutions.

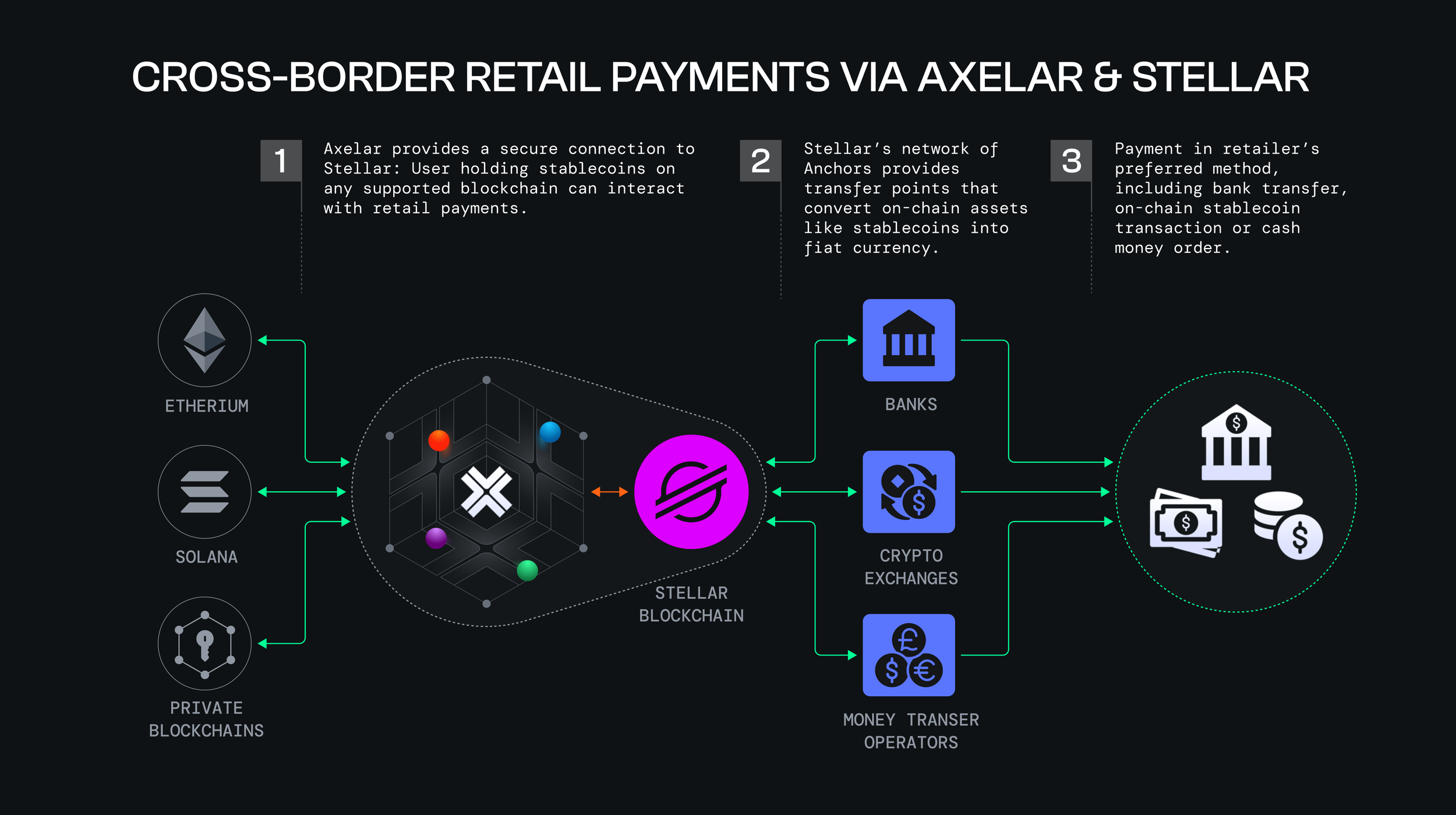

Stellar, launched in 2014, is a decentralized blockchain designed specifically for global payments and everyday financial services for consumers and merchants. Its native cryptocurrency, Lumens (XLM), serves as a bridge currency to facilitate currency conversions and reduce transaction costs. Key innovations include:

Speed and cost efficiency: Stellar transactions settle in 3–5 seconds, with fees as low as fractions of a cent, compared to traditional cross-border payments that can take days and incur high fees. This makes Stellar ideal for retail use cases like remittances and micropayments.

Anchors and asset issuance: Stellar’s “anchors” are trusted entities (e.g., banks or payment providers) that issue digital representations of real-world assets, such as fiat currencies or stablecoins, on the Stellar ledger. This allows users to transact in familiar currencies while leveraging blockchain’s efficiency.

Built-in decentralized exchange: Stellar’s integrated decentralized exchange (DEX) enables seamless currency conversion, allowing a user to pay in USD and a merchant to receive EUR without manual intervention. This mirrors the automatic currency conversion in traditional payment networks.

Interoperability focus: Stellar’s design emphasizes connectivity with external systems. Its open APIs and compliance with standards like ISO 20022 enable integration with traditional financial institutions and payment processors. Partnerships with companies like MoneyGram International and Flutterwave showcase Stellar’s ability to bridge blockchain and legacy systems, enabling merchants to accept payments globally with minimal infrastructure changes.

Stellar’s approach illustrates how blockchain can replicate the speed and accessibility of traditional retail payments while addressing pain points like high fees and slow settlement. However, its success in retail payments depends on broader blockchain interoperability to connect disparate networks and integrate with existing payment ecosystems.

The Need for Decentralized Blockchain Interoperability in Retail Payments

The fragmented nature of blockchain ecosystems—where Bitcoin, Ethereum, Stellar and countless others operate with distinct protocols, consensus mechanisms and asset standards—poses a significant barrier to seamless retail payments. A consumer using a Bitcoin wallet cannot easily pay a merchant on Ethereum, nor can either interact effortlessly with a Visa-compatible point-of-sale system without complex solutions. To achieve the frictionless experience of traditional retail payments, blockchain interoperability is essential, both among blockchain networks and with legacy payment systems. However, current interoperability solutions often introduce risks that undermine their suitability for retail payments, necessitating decentralized alternatives like Axelar.

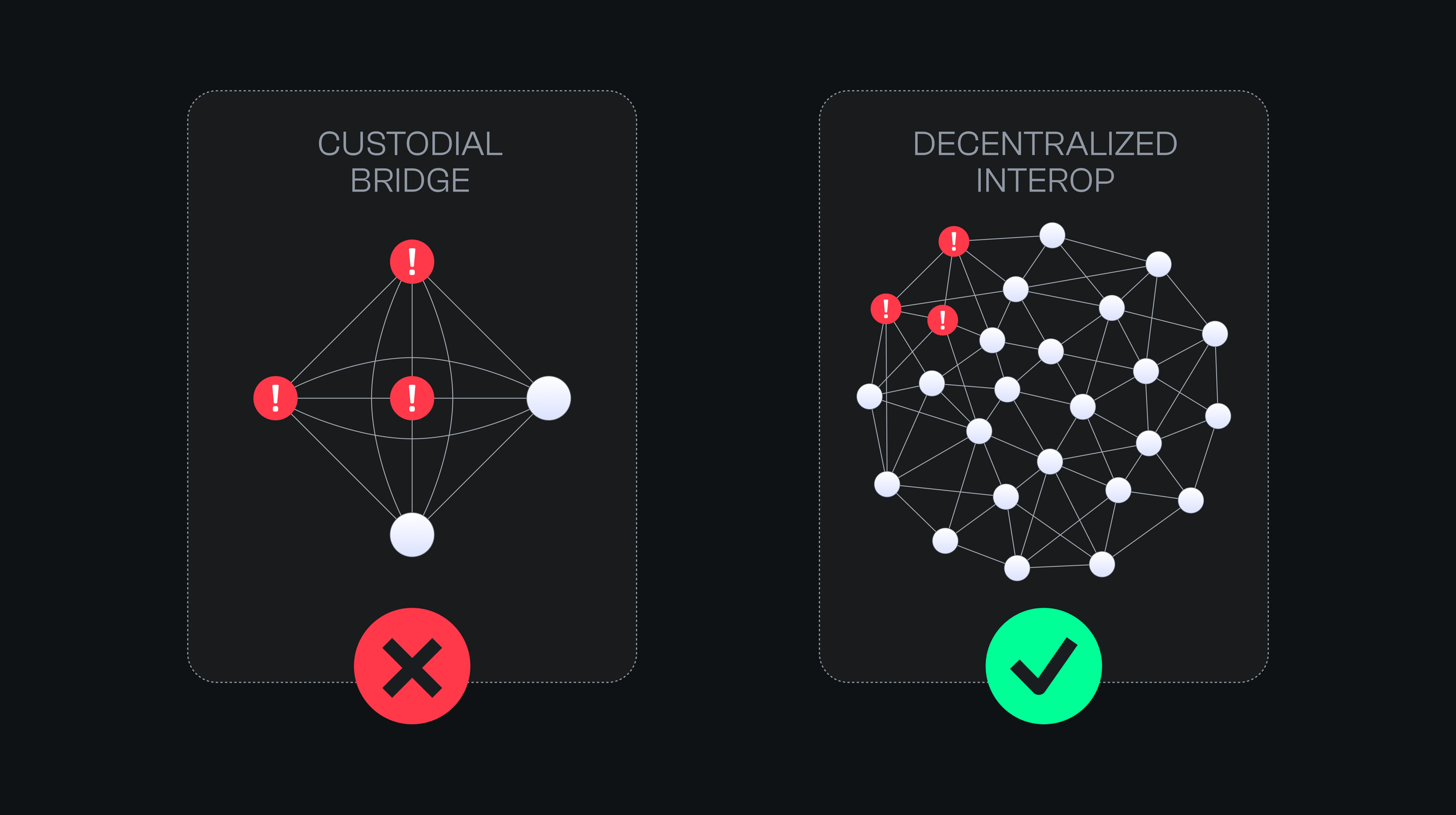

A variety of interoperability protocols and blockchain-specific bridges exist to facilitate the basic task of moving assets between blockchains. However, many existing bridges and connectors are custodial and closed-source, meaning a single entity or a small group of entities controls the funds during transfer. This centralized control introduces significant security and operational risks, particularly for retail payment systems that require trust and reliability.

Custodial bridges have proven vulnerable to catastrophic cyberthefts, with two of the largest known cybercrimes in any industry targeting such systems. In March 2022, the Axie Infinity Ronin Bridge was hacked, resulting in the theft of $625 million in cryptocurrency. The breach occurred when attackers compromised the centralized validator nodes operated by Sky Mavis, the company behind Axie Infinity, exploiting the bridge’s custodial design. Similarly, in February, 2025, the Bybit crypto exchange, another centralized organization engaged in transactions involving multiple decentralized blockchains, suffered a hack with losses estimated at nearly $1.5 billion. These incidents highlight the fragility of custodial connectors, where a single point of failure can lead to massive financial losses, eroding trust in blockchain-based payment systems.

Beyond security, custodial and closed-source interoperability solutions pose a risk of vendor lock-in, a critical concern for payments networks. Closed-source systems limit transparency and restrict merchants or developers from adapting or auditing the technology. This can lead to dependency on a single provider, stifling innovation and increasing costs over time. For retail payments, where flexibility and competition drive efficiency, such lock-in undermines the scalability and accessibility needed for widespread adoption.

In contrast, decentralized interoperability protocols like Axelar offer a promising alternative. Axelar facilitates cross-chain communication through a decentralized network of nodes, enabling secure and transparent asset transfers without relying on a single controlling entity. Unlike custodial bridges, Axelar disperses control across its network, reducing the risk of centralized vulnerabilities and fostering trust for retail payment use cases.

Decentralized interoperability, as exemplified by Axelar, operates according to several key principles:

Independent node network: Asset and message transfers are executed by a network of nodes that operate separately from the connected blockchains, ensuring no single blockchain’s failure compromises the interoperability layer.

Non-custodial design: The software components of the network are non-custodial, with control distributed across the node network, eliminating reliance on a single entity to hold or manage funds.

Open participation: The infrastructure is open to public participation, governed by rules encoded in the network’s software. Control over changes to these rules is distributed across the network, preventing centralized dominance.

Decentralized governance: Network operations and protocol updates are governed non-centrally, with decision-making power spread across the network’s participants, ensuring fairness and adaptability.

Transparent ledger: All transaction data, including addresses, fees and routing information, is recorded on a public blockchain ledger, providing full transparency and auditability for users and merchants.

These principles ensure that decentralized interoperability protocols like Axelar can support retail payments with the security, transparency and flexibility required to rival traditional systems. By mitigating the risks of custodial bridges and vendor lock-in, decentralized solutions pave the way for a payments ecosystem where consumers can pay with any cryptocurrency or tokenized asset, on any blockchain, at any merchant—whether they accept crypto or fiat—without encountering technical or operational barriers.

Conclusion: Unlocking the Future of Retail Payments

The interoperability of traditional retail payments—where payment instruments, networks and processors work in harmony—sets a high bar for blockchain-based solutions. Innovations like Stellar’s low-cost, high-speed payment infrastructure show that blockchain can compete with and even surpass traditional systems in efficiency and accessibility. However, the fragmented nature of blockchain ecosystems remains a significant hurdle. By prioritizing interoperability within and beyond blockchain networks, the industry can deliver a payment experience that rivals the seamlessness consumers expect today.

Bitcoin Pizza Day, May 22, is the anniversary of the first-ever commercial transaction using bitcoin: In 2010, Bitcoin contributor Laszlo Hanyecz bought two pizzas for 10,000 bitcoin. As we celebrate Bitcoin Pizza Day in 2025, the dream of a global, decentralized payment system is within reach – but only if we build bridges to connect the islands of innovation in the blockchain world. With interoperable systems, the next pizza purchase could be as simple as a tap, whether paid in XLM, BTC, or USD, on any network, anywhere in the world.